1×9 adjoint(::Vector{Float64}) with eltype Float64:

0.0 0.375 0.75 1.125 1.5 1.875 2.25 2.625 3.0Machine Learning for Computational Economics

Module 02: Discrete-Time Methods

EDHEC Business School

January 2026

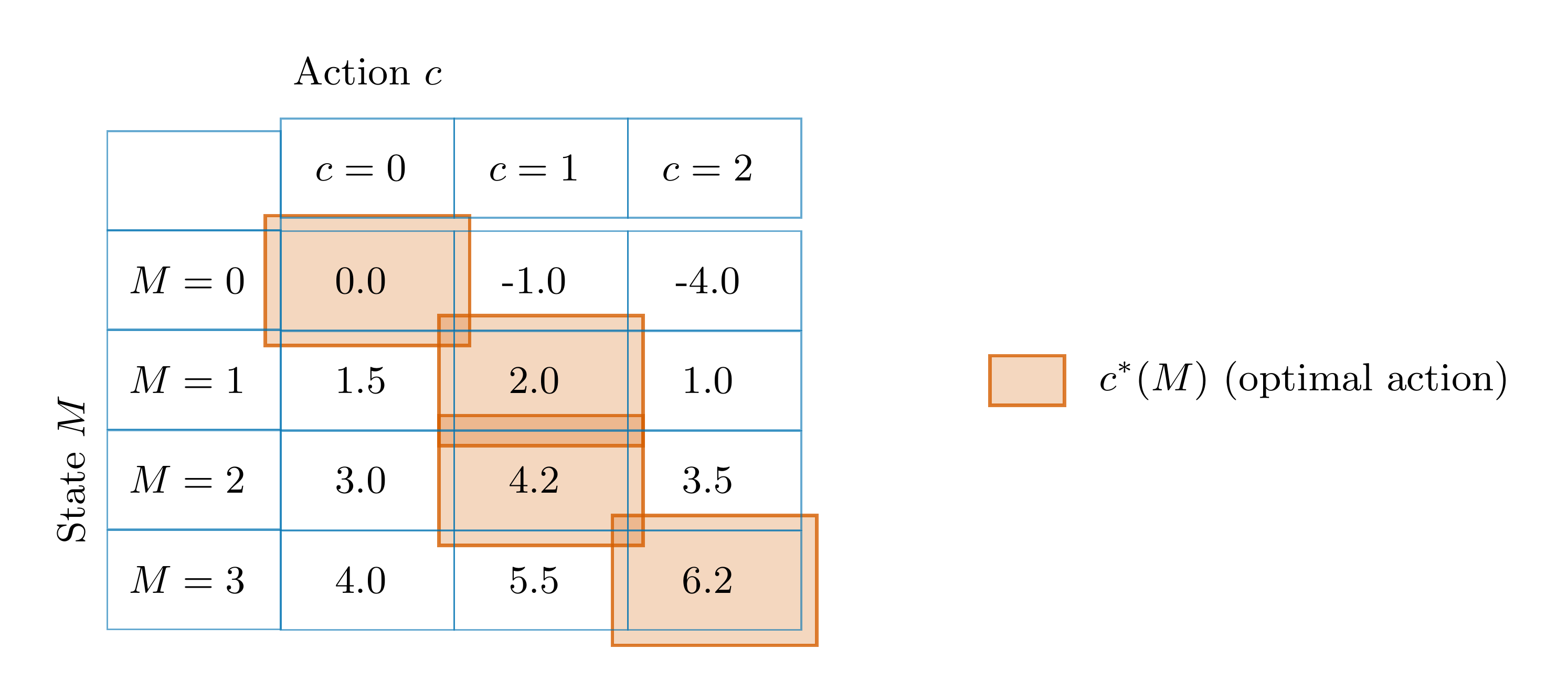

The Action-Value Function

The action-value function is given by \[ V_t(M, c) \equiv u(c) + e^{-\rho} \mathbb{E}\!\left[ V_{t-1}(R (M- c) + Y') \right]. \]

Tip

The action-value function corresponds to the value associated with a given action (no maximization step).

Think of \(V_t(M,c)\) as a table

- Columns: actions \(c\)

- Rows: states \(M\)

Optimal consumption: \[c_t(M) = \arg\max_{c} V_t(M,c)\]

Accuracy of a Linear Interpolation

The accuracy of a linear interpolation depends on the grid size.

- We can approximate even very non-linear functions this way.

- Depending on the function, this may require a very fine grid.

Quality of approximation may not be uniform

- Worse approximation near the boundaries.

Uniform grid can be very inefficient

- It does not allow to focus where it is needed

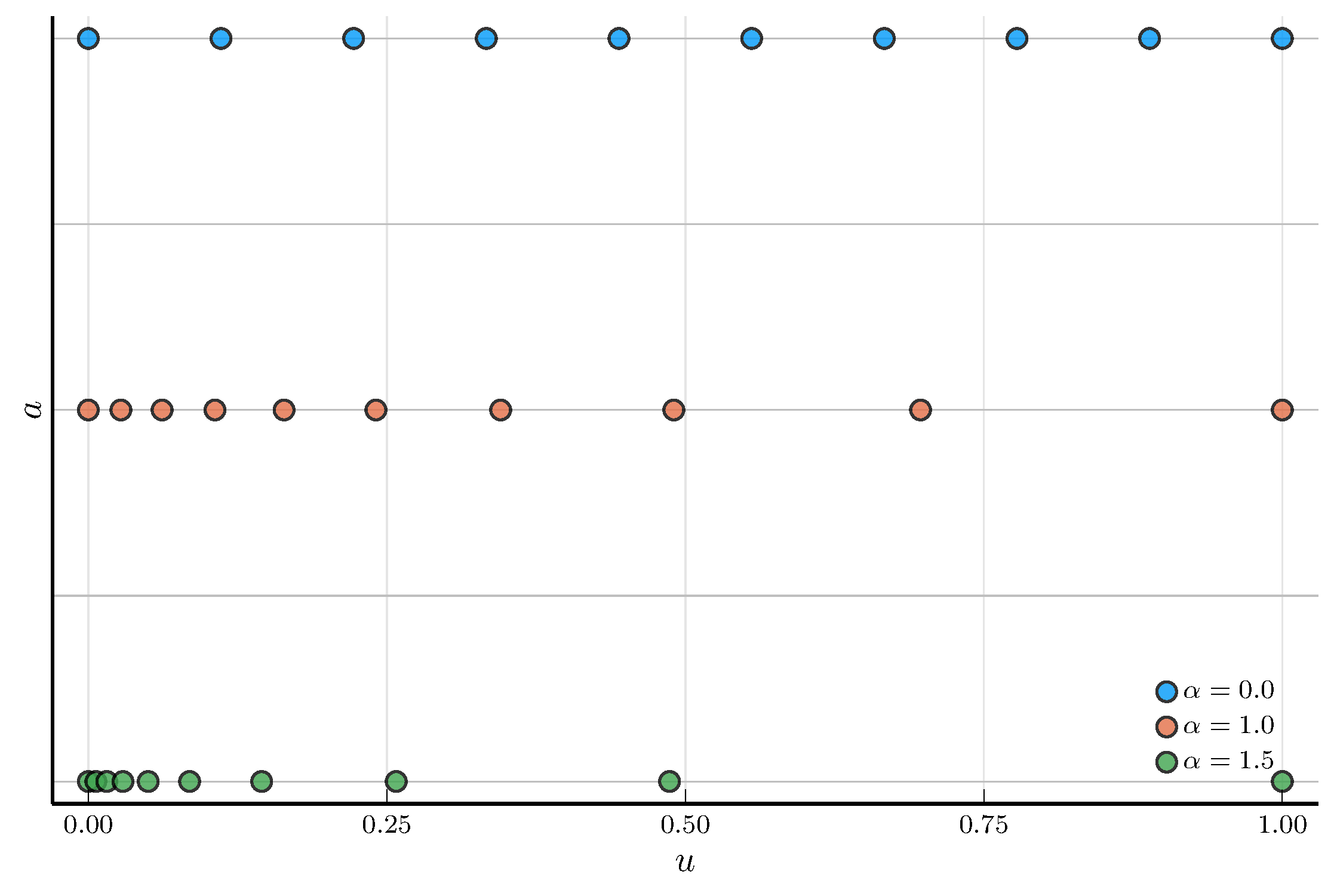

Non-Uniform Grids

An alternative is to use a non-uniform grid for the state variable.

A convenient choice is the double-exponential grid

- Clusters grid points near the lower bound.

- Let \(u^j\) denote a uniform grid on the unit interval \([0,1]\).

- Define the grid points as \[ a_j = a_{\min} + (a_{\max} - a_{\min}) \frac{e^{\,e^{\alpha u^j}-1} - 1}{e^{\,e^{\alpha}-1} - 1}, \]

The parameter \(\alpha > 0\) controls the degree of clustering.

- As \(\alpha \to 0\), the grid becomes approximately uniform.

- For large \(\alpha\), the grid is very dense near the lower bound.

We can implement this in Julia as follows:

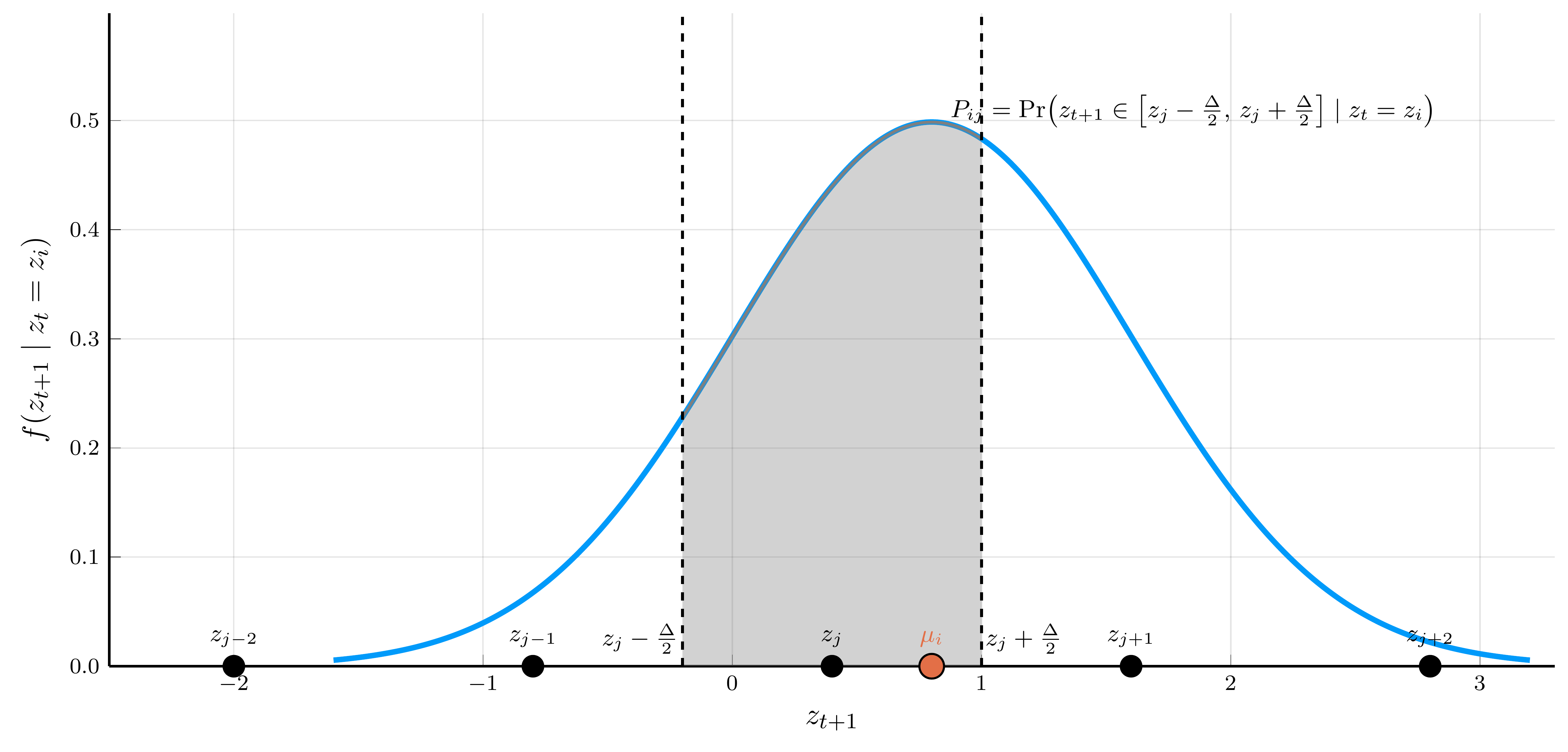

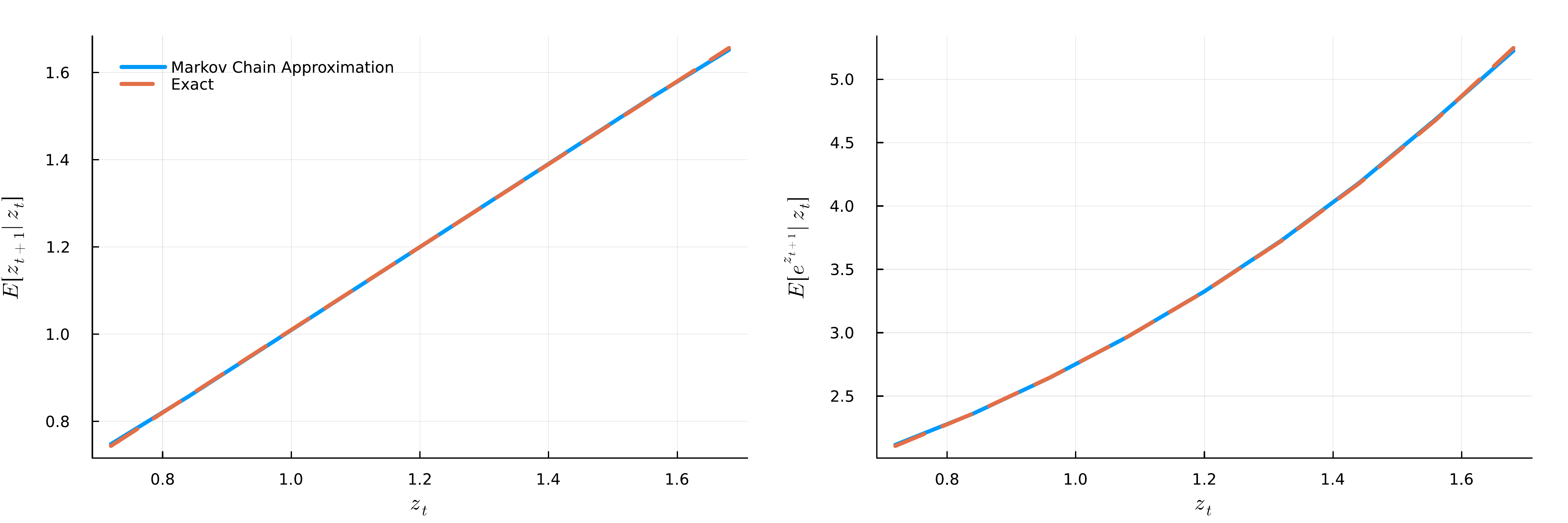

The Tauchen Method: Computing the Transition Probabilities

We need to determine the transition probabilities \(P_{ij} = \Pr(z_{t+1} = z_j \mid z_t = z_i)\).

- Conditional on \(z_t = z_i\), we have that \(z_{t+1} \sim \mathcal{N}\left(\mu + \rho_z (z_i - \mu), \sigma_\varepsilon^2\right)\).

The transition probability \(P_{ij}\) equals the probability that \(z_{t+1}\) falls between the midpoints surrounding \(z_j\):

\[\scriptsize P_{ij} = \begin{cases} \Phi\!\left(\dfrac{z_j - \mu_i + \tfrac{\Delta}{2}}{\sigma_\varepsilon}\right), & j = 1, \\[0.75em] \Phi\!\left(\dfrac{z_j - \mu_i + \tfrac{\Delta}{2}}{\sigma_\varepsilon}\right) - \Phi\!\left(\dfrac{z_j - \mu_i - \tfrac{\Delta}{2}}{\sigma_\varepsilon}\right), & 1 < j < N_z, \\[0.75em] 1 - \Phi\!\left(\dfrac{z_j - \mu_i - \tfrac{\Delta}{2}}{\sigma_\varepsilon}\right), & j = N_z, \end{cases} \]

Conditional Moments: Exact vs. Markov Chain Approximation

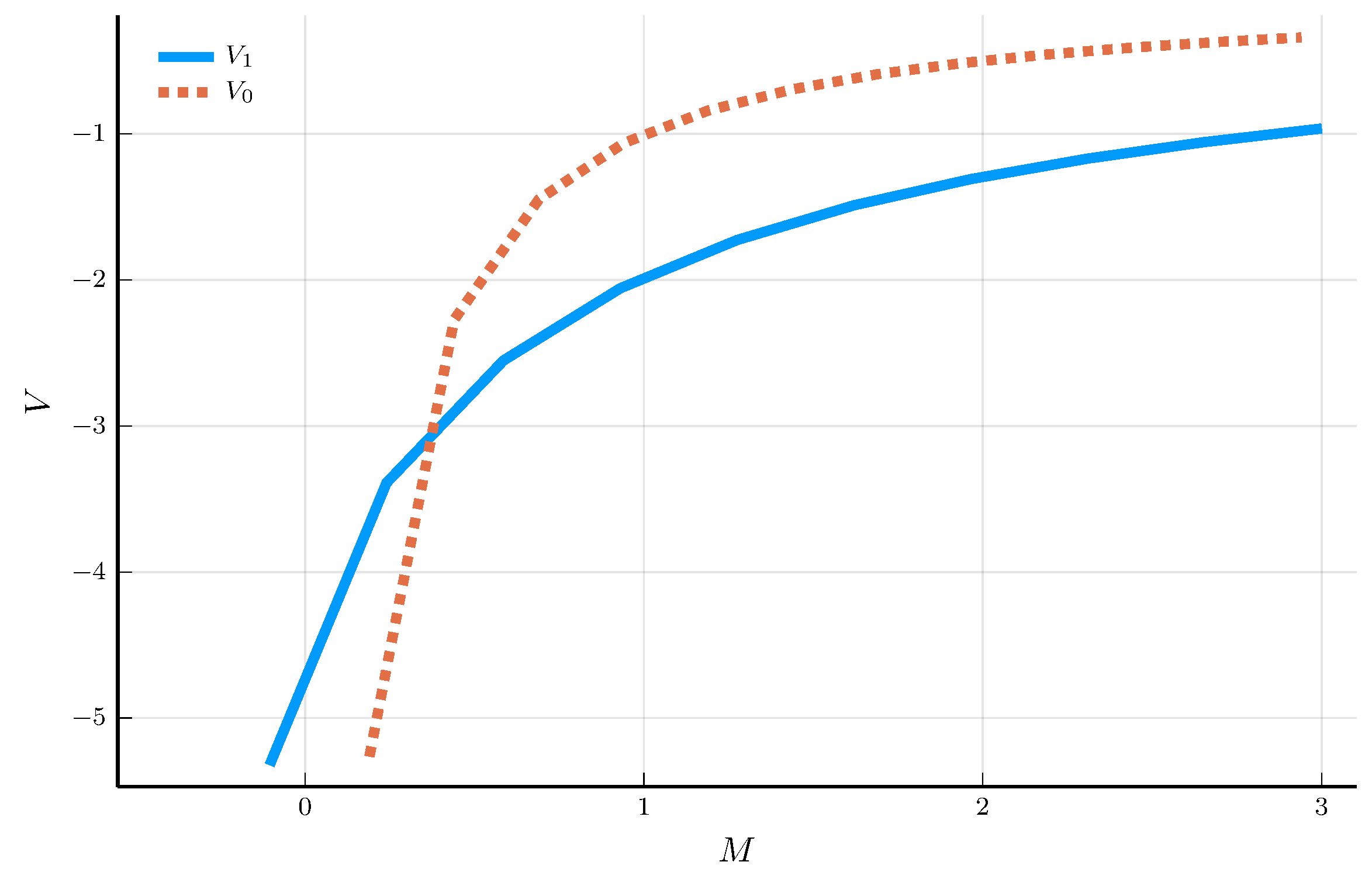

Policy and Value Functions

Two theoretical bounds for the policy function:

Lower bound: household receives the lowest income with certainty.

Upper bound: household receives the average income with certainty.

a) Policy functions

b) Value functions

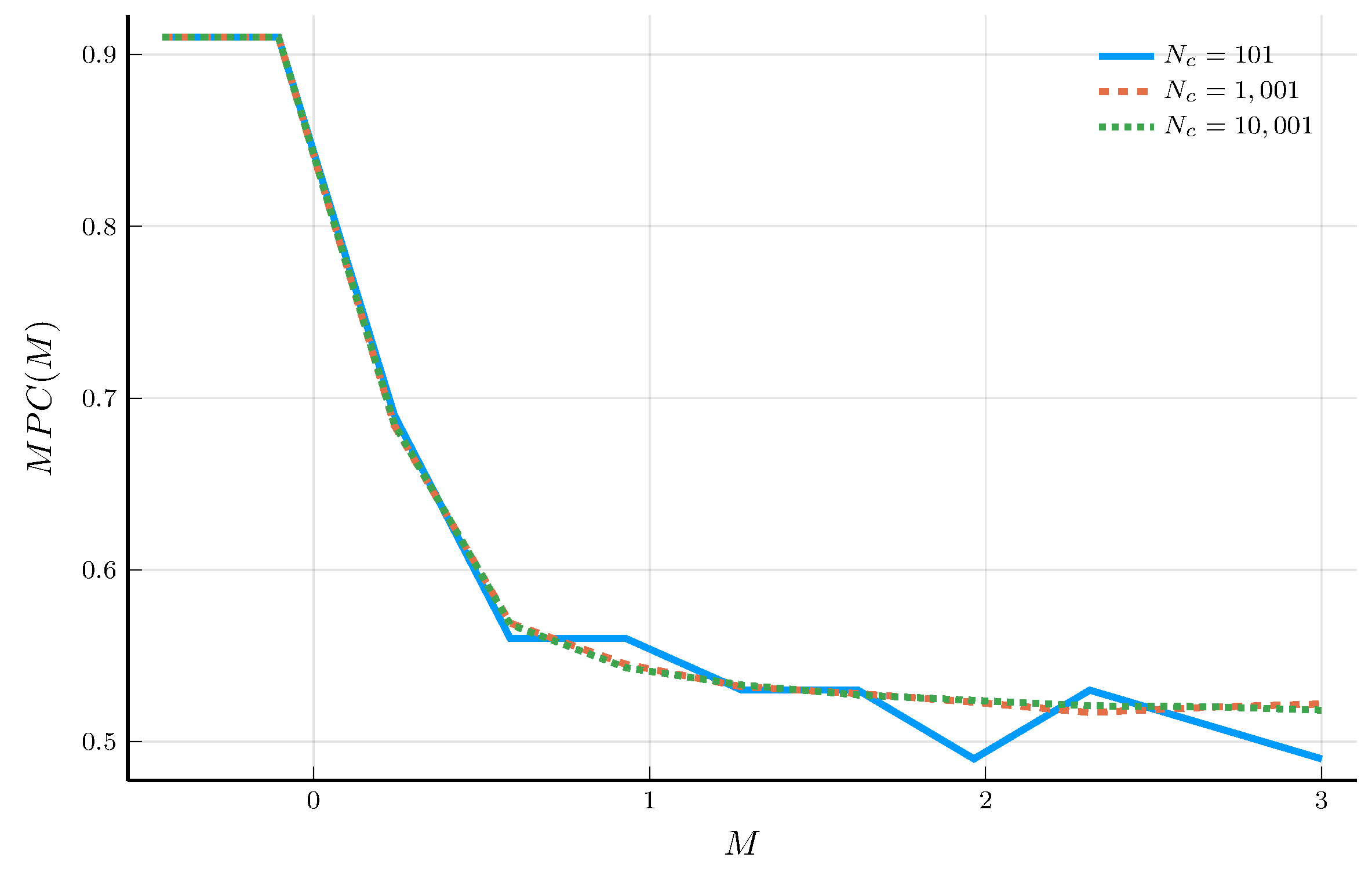

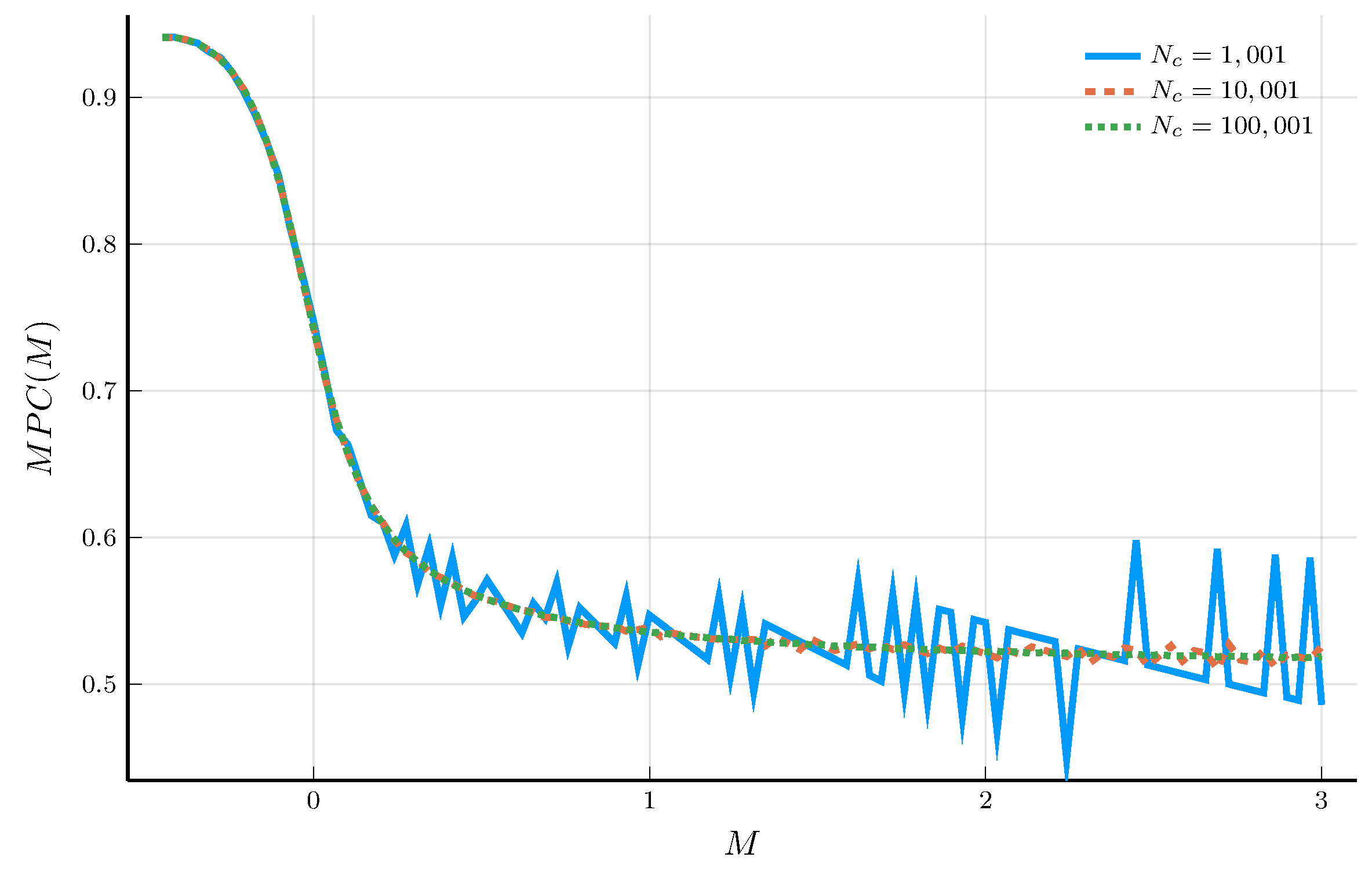

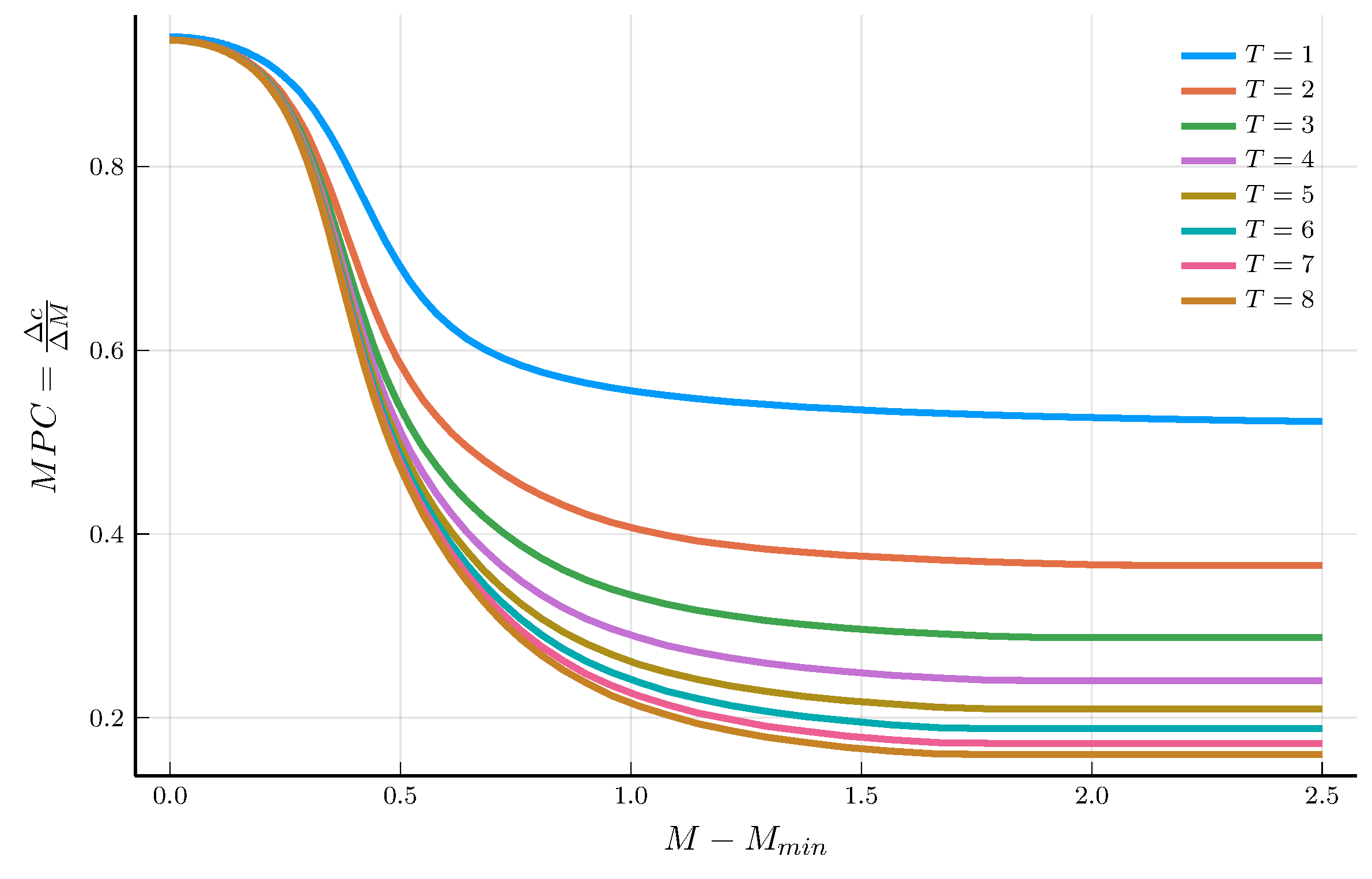

The Marginal Propensity to Consume

Given the policy function \(c_t(M)\), we can obtain the marginal propensity to consume (MPC).

- The MPC measures the change in consumption for a change in \(M\): \(MPC(M) = \frac{d c_t(M)}{d M}\).

Carroll and Kimball (1996) show that the MPC is decreasing in \(M\).

- But the numerical solution does not necessarily satisfy this property.

a) MPCs for \(N_M = 11\)

b) MPCs for \(N_M = 101\)

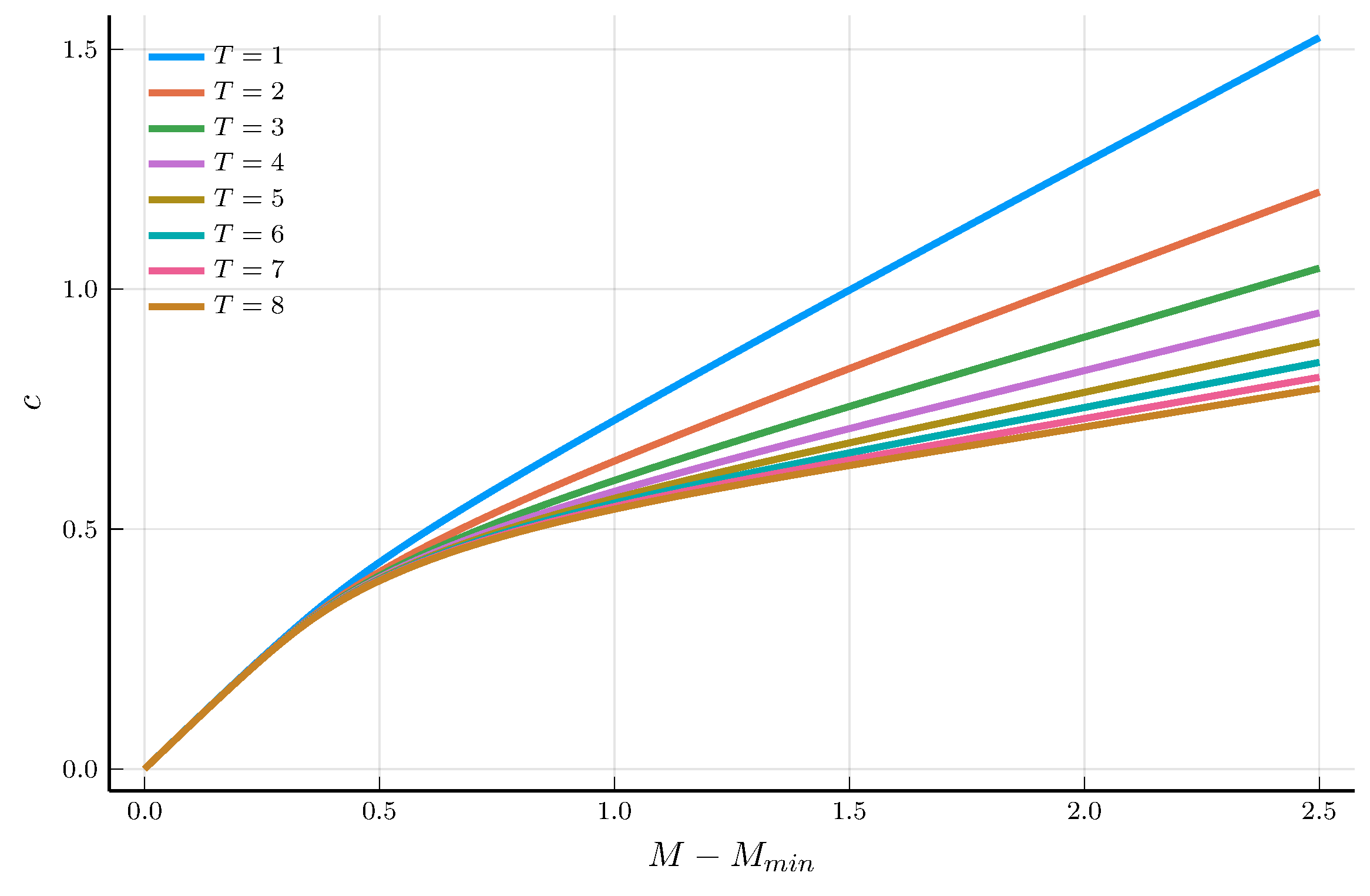

The EGM Iteration

We iterate the EGM step until the policy function converges.

We can compute the marginal propensity to consume (MPC) using the finite-difference method.

a) Policy function

b) Marginal propensity to consume